Asc 360-10 property plant and equipment. ASC 360 Property, Plant, and Equipment 2019-05-09

ASC 360 Property, Plant, and Equipment

Depreciation of Equipment Generally accepted accounting principles require that the cost of assets that are expected to be useful for greater than a year be spread over the expected life of the asset. If C a loss is recognized 6. Property, plant, and equipment are some of the most significant items in the statement of financial position and usually represent a substantial investment by the entity. However, is it essential that the use of a threshold does not materially affect the financial statements. Among other topics, the publication discusses 1 implementation issues related to the guidance on measurement of credit losses on financial instruments, 2 the issuance of targeted improvements to hedge accounting, and 3 application of the new revenue recognition and leasing standards. For some intangible assets, the business can expect to receive the benefit of the asset for the life of the business. Entities use historical cost to value property, plant, and equipment.

Property, Plant and Equipment, ASC 360

In these cases, amortization is not performed, but instead the company determines if the asset is still as valuable as the cost carried on the accounting records. Related resources See our comprehensive of news and publications related to property, plant, and equipment. Accounting standards require that inventory is carried in the accounting records at the lower of cost or market value. Small business owners are free to choose a method that works for them. Long-lived assets held for sale 2. For example, a company's trademark may not have a definite life.

Accounting Standards Relating to Depreciation & Inventory

The substitute plant method assumes that a modern plant or plants would replace an existing plant or plants of the same or similar capacity, and that the value of the existing plant would be equivalent to the capitalized value of the difference between the operating annual operating costs and fixed charges of the modern substitute and the annual operating costs of the existing plant. Revaluation decreases are recognized in profit or loss unless they reverse a previous revaluation increase. September 2018 update to the Property, plant, equipment and other assets guide Certain updates to reflect changes due to recent standard setting activity and to add new interpretive guidance have been made. Inventory Valuation Even though inventory is recorded at cost upon purchase, the work of the accountant may not be done. The recorded amount of an asset includes all of the costs necessary to get the asset set up and functioning properly for its intended use, including interest. Determination of costs is critical to proper accounting for property, plant, and equipment.

Accounting Standards Relating to Depreciation & Inventory

Presented separately in the statement of financial position 2. All direct costs of constructing an entity's own tangible fixed assets are capitalized. Jan 24, 2018 The January 2018 edition of our annual update highlights selected accounting and reporting developments that may be of interest to entities in the insurance sector. In this section, small business owners will find that, in general, inventory purchases should be recorded at cost. Understanding where guidance related to inventory and depreciation, two topics common to small business, are located can save you, and your accounting staff, both time and money. Below is an overview of each Subtopic. The method should be considered by all electric utilities, including companies not operating in ''fair value'' jurisdictions.

ASC 360 Property, Plant, and Equipment

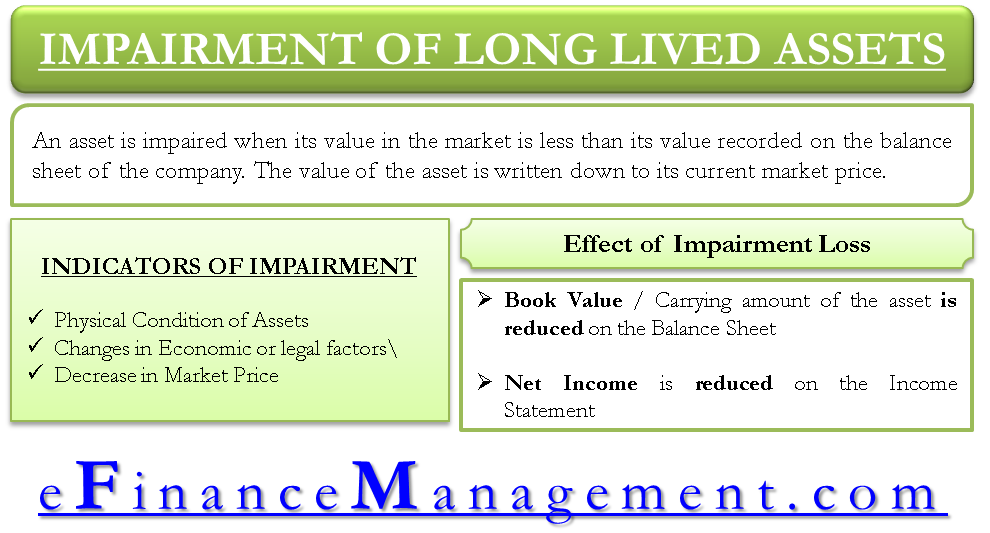

Depreciation is meant to allocate the cost of an asset over the period it is in use by the reporting entity. Please see to learn more about our global network of member firms. Impairment of long-lived assets 3. This Subtopic also includes guidance on the impairment or disposal of long-lived assets. Upon acquisition, the reporting entity should measure and capitalize all the historical costs necessary to deliver the asset to its intended location and prepare it for its productive use.

ASC 360 Property, Plant, and Equipment

When estimating the useful life of an asset, entities should consider all relevant facts and circumstances. Property, Plant and Equipment are tangible assets and are expected to be used during more than one period generally more than one year. . This means that if inventory isn't worth as much as it was originally paid for, then the company must make an adjustment in the accounting records to reflect that change. The amount is based on the difference between the carrying value and the fair market value is what is actually booked. See Appendix D, Summary of significant changes, for information on the most recent updates. The difficulty arises in determining how to allocate different costs and charges to goods being produced.

Accounting for PPE: IAS 16 / ASC 360

They are not for resale. Policies for recording cost, capitalization, assigning useful lives, and depreciation are summarized below. Costs incurred to replace Property, Plant, and Equipment or to enhance the productivity of a long-lived asset should also be capitalized. The historical cost is the amount of cash or cash equivalents paid for an asset. Amortization of Intangible Assets When the costs of intangible assets, such as patents or software agreements, are spread over the useful life of the asset, this process is known as amortization.

Accounting for PPE: IAS 16 / ASC 360

Impairment or disposal of long-lived assets, which contains guidance for: recognizing impairment of long-lived assets to be held and used, long-lived assets to be disposed of by sale, and disclosures for the implementation and disposals of individually significant components of an entity. When selecting a method, consideration should be given to the cost of repairs and maintenance, whether productivity declines over time, and if the asset may become obsolete quickly. Lastly, the section informs financial statement preparers that there are many acceptable manners in which to determine the cost of inventory. Income tax depreciation differs in amount from financial statement depreciation because of differences in treatment of salvage value, recovery methods, recovery periods, and the use of conventions for assets placed in service during the year. This is most common in industries where product spoilage or technological obsolescence are common. Jan 15, 2016 The eighth annual accounting and financial reporting update discusses topics that may be of particular interest to real estate entities.

Chapter 25: ASC 360 PROPERTY, PLANT, AND EQUIPMENT

Costs that are not required to prepare an asset for use, such as regular maintenance, should be expensed as incurred. Please see to learn more. Items of property, plant, and equipment are used in the ordinary course of business. The costs of property, plant, and equipment are allocated tithe periods of their expected useful life through depreciation or depletion. Note: in all 3 exceptions the carryover basis book value or carrying amount adjusted for cash paid or received as part of the transaction is used to measure the transaction instead of the fair value.

Chapter 25: ASC 360 PROPERTY, PLANT, AND EQUIPMENT

About the Author John Freedman's articles specialize in management and financial responsibility. Measured at the lower of B and C B carrying amount C fair value less cost to sell 4. He is a certified public accountant, graduated summa cum laude with a Bachelor of Arts in business administration and has been writing since 1998. Introduction Almost any type of companies engaged in various businesses need capital assets to use in the production or supply of goods or services, or for administrative purposes e. The section also acknowledges that accounting for inventory can be difficult, especially for manufacturers. Dec 22, 2017 The 2017 edition of our annual update highlights selected accounting and reporting developments that may be of interest to entities in the banking and securities sector. However, whatever manner is chosen, it must be consistently applied.