Customer product profitability analysis. Customer profitability analysis for better decisions 2019-03-12

Customer Profitability Analysis: Definition & Examples

Revisit your channel strategy One of the key reasons customers are unprofitable is because the costs of doing business with them is out of step with their potential for profit. All too often, these large accoprounts have such bargaining power that they already enjoy large discounts and generous payment terms. When going through these steps, you will need to make numerous modeling decisions and overcome unanticipated roadblocks. You also need to allocate all of your promotional expenses, discounts, allowances, rebates and returns to the sales. Data can also be revaluated periodically to adjust the initial, real-time valuation or add the actual costs of goods manufactured. An analysis may need some persuasion from management to see potential benefits. The first step in analyzing customer profitability is to sort your annual sales by customer in descending order.

Customer Profitability Analysis: Definition & Examples

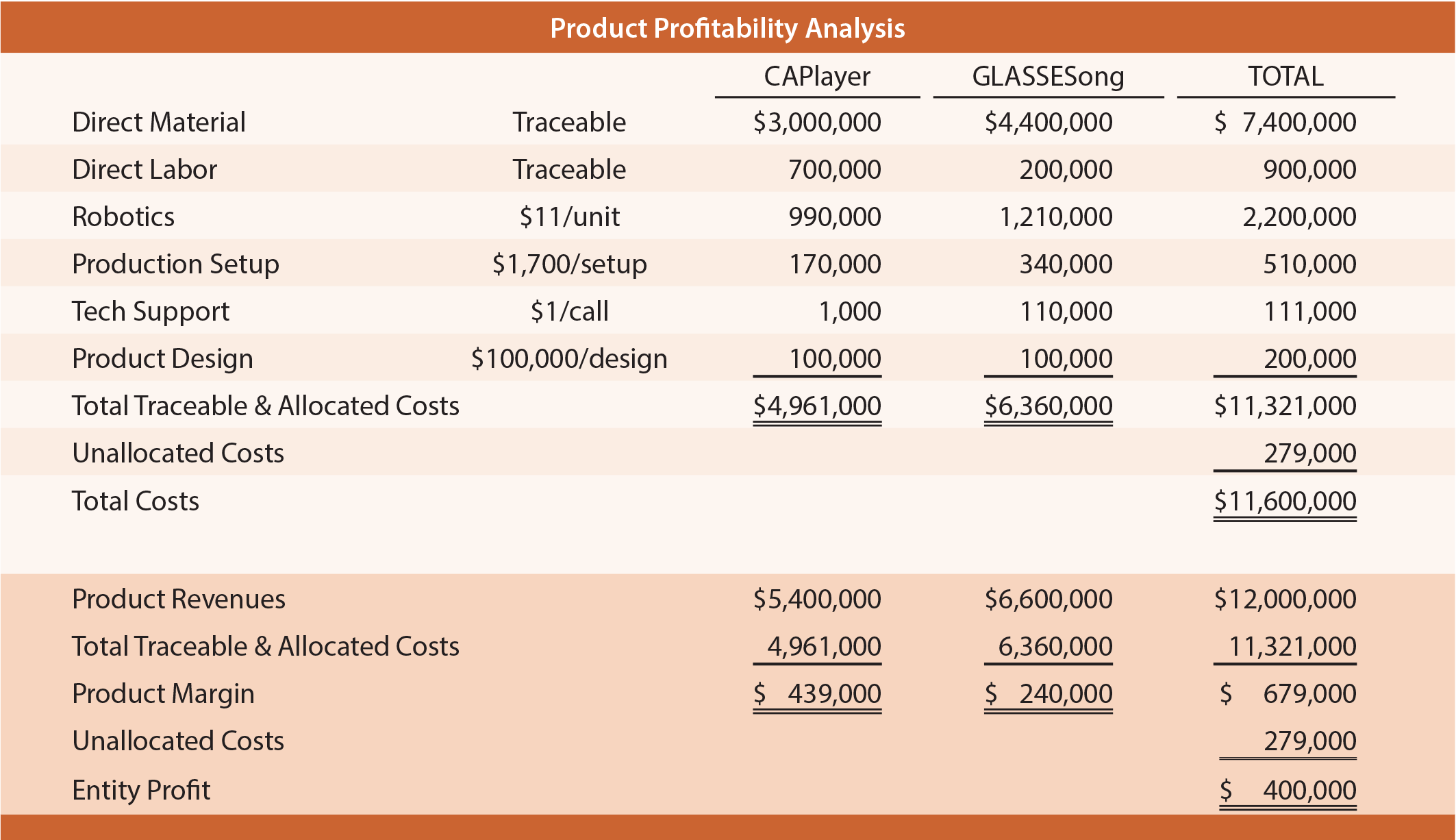

Thus, this method emphasizes on summarizing the activity and situational change over a period of time, for a given organizational unit. If the current pricing does not allow the organization to reach its target profitability, the answer may be to: a increase price in segments with low price elasticity, b discontinue a product or business, c consider not serving a particular customer segment, or, d look for other efficiencies. Rework your discounting policy Knowing how net profitability varies with customer size gives you important insights that once paired with data about product profitability will help you formulate a commercially driven discounting policy. Standard costs can be used to valuate the cost of sales for the purpose of obtaining a preliminary profit analysis. Costing-Based Profitability Analysis This type of Profitability Analysis is primarily designed to allow analysis of profit quickly for the purpose of sales management. Also ensure that your customer contact teams are aware of which group of customers are the most valuable to the business. Adjustments to the price paid by the customer for a product or service, such as discounts, service fees or product enhancement fees, must be included to determine the true amount of revenue generated by each customer and the aggregated amount calculated for the customer segment.

What is profitability analysis?

The method of determining period operating results in Profitability Analysis is based on the assumption that a company's success can be measured primarily on the basis of its transactions with other companies. Divi is a senior banking practice expert at , a strategic management consulting firm with offices in San Juan, Puerto Rico and Miami. For an even more sophisticated analysis, you can apply only your variable costs to the sales. These costs may include, for example, engineering or design costs, special manufacturing equipment and practices, or even invoicing and collection. In a first step, the characteristics have to be defined for the operating concerns.

Profitability Analysis General Overview

A business can also focus effort on retention, or holding on to existing clients, of the more valuable customers in the base, because it's usually easier to keep customers than find new ones. In addition, their margins are lower as they receive the best interest rates in both credit and deposit products, and fees related to their credit cards and deposit accounts are often waived. As revenue increases, more resources are required to produce the goods or service. This review is necessary because there may be some cost types that have been included in product costs that are related more to the customer than to a product. Both of these applications can be used -- and consequently both methods--at the same time in your organization.

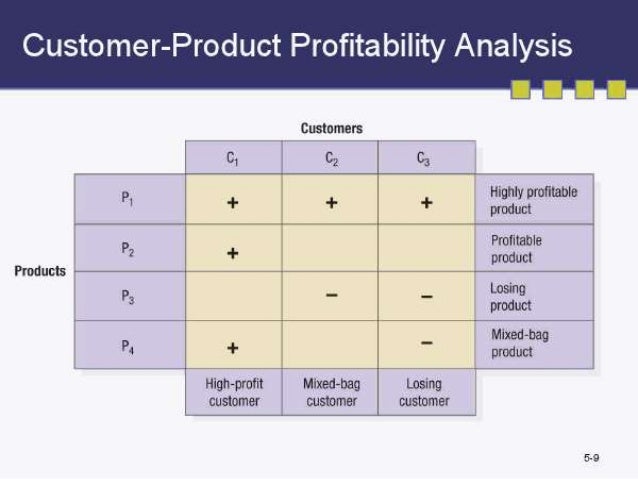

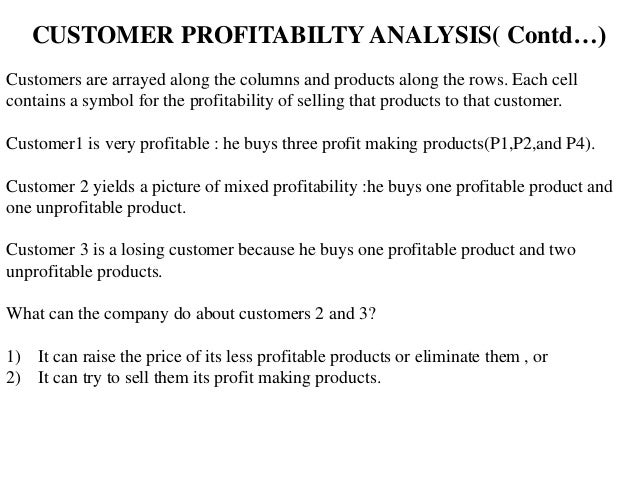

Customer and Product Profitability Analysis

Their definition applies to all clients. Is your financial institution capable of answering questions related to the profitability of its customer base? There are a lot of reasons why companies keep depending on big customers and having them in their portfolio. Companies are enamored with rolling out new products and satisfying customer demand, however not all products contribute equally. You might need to make subpar business decisions because the customer holds all the bargaining chips. If a profitability software package is not within reach, know that you can use an application like Microsoft PowerPivot to build a very robust and flexible product profitability model at the account level, especially if the bank has solid account and transactional databases. Get rid of those customers.

Customer and Product Profitability Analysis

For more detail of what this could look like and key insights regarding advanced decision making in every part of your business, register for one of our. If a certain customer is responsible for 60% of your earnings, you're in serious trouble because you'll spend so much time servicing them that you won't have the time to find other customers and diversify risk. A startup customer may not be profitable now, but once they take off, you'll be sorry you lost them. This means that there are 4 times as many customers in this lower-value group that consume much of your time and resources. Otherwise, it can look to charge its customers for additional service visits to shift the weight of the cost from the company to the customer. Your Problem You need to compare the profitability of various products in your portfolio.

What is Customer Profitability Analysis? (with pictures)

Many businesses use a customer as a means of streamlining processes so they provide the highest degree of efficiency and return, while generating the lowest degree of cost. Sometimes the costs may be indirect. Therefore, activity-based costing considers all these potential activities looks at the various Fixed and Variable Costs Fixed and variable costs are important in management accounting and financial analysis. You should be spending your time developing more sales with these customers and enhance your relationship. Breaking down the task into segments makes it much easier to identify what is actually working to increase profitability with a major client or a group of clients within the customer base, as well as what elements may be inhibiting the potential for earning more revenue from those same clients.

Customer profitability analysis for better decisions

It represents a competitive advantage with meaningful short- and long-term returns. Criticism of Customer Profitability Analysis The biggest criticism regarding Customer Profitability Analysis is the selection of a limited timeframe and segmentation criteria. In those cases, management may establish a minimum loan amount in their underwriting policy, charge a higher price or higher underwriting fees, or create an expedited and less expensive underwriting process. By obtaining this information as a model input you will guarantee that this allocation is acceptable to the highest stakeholders. .